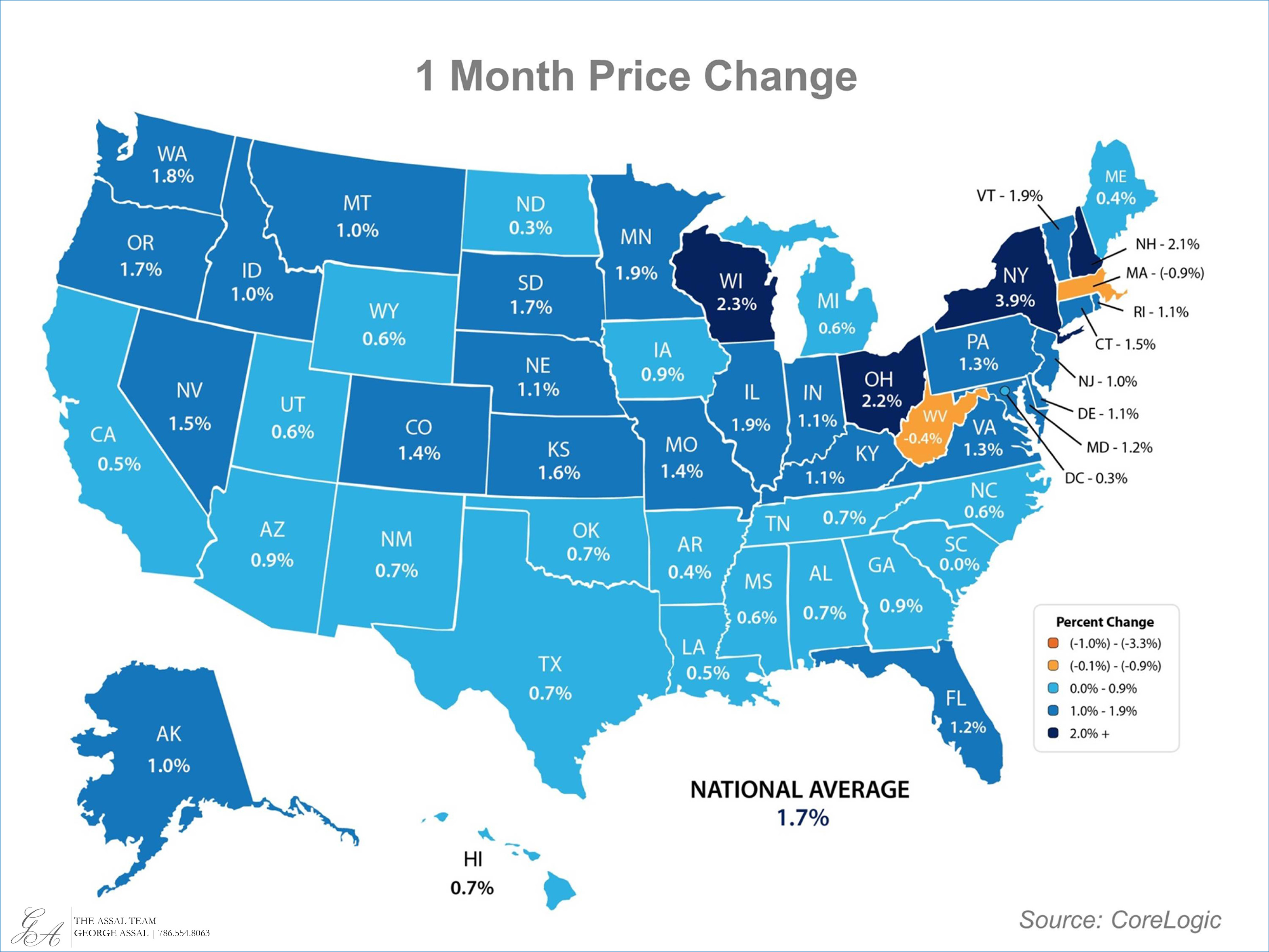

There is no doubt that home prices in the vast majority of housing markets across the country are continuing to increase on a month over month basis. The following map (based on data from the latest CoreLogic pricing report) reveals the appreciation level by state:

These increases in value have caused some to be concerned about a new price bubble forming in residential real estate. Here are quotes from many of the most respected voices in the housing industry regarding the issue:

Nick Timiraos, reporter at the Wall Street Journal:

“Predictions of a new national home price bubble look unfounded for now, according to data.”

Michael Fratantoni, Chief Economist, the Mortgage Bankers Association:

“I don’t really see it as a bubble.”

Jack M. Guttentag, Professor of Finance Emeritus at the Wharton School of the University of Pennsylvania:

“My view is that we are a long way from another house price bubble.”

Rajeev Dhawan, Director of Economic Forecasting Center at J. Mack Robinson College of Business, Georgia State University:

“To have a bubble, you need to have construction rates higher than the perceived demand, which is what happened in 2003 to 2007. Right now, however, we have the reverse of that.”

Victor Calanog, Chief Economist, Reis:

“The housing market has yet to show evidence of systematic runaway asset price inflation characterized by home prices rising much faster than household income.”

David M. Blitzer, Chairman of the Index Committee for S&P Dow Jones:

“I would describe this as a rebound in home prices, not a bubble and not a reason to be fearful.”

Andrew Nelson, US Chief Economist, Colliers International:

“I don’t think there is a housing bubble.”

George Raitu, Director, Quantitative & Commercial Research, NAR:

“We do not consider the current market conditions to present a bubble.”

Christopher Thornberg, Founding Partner, Beacon Economics:

“The housing market is far from overheated.”

So why have prices been increasing?

Today, there is a gap between supply (number of houses on the market) and demand (the number of buyers looking for a new home). In any market, this would cause values to increase. Here are some experts’ comments on this issue:

Jonathan Smoke, realtor.com Chief Economist:

“So does that mean we’re in a bubble? Nope, that’s just what happens when demand increases faster than supply.”

Robert Bach, Director of Research – Americas, Newmark Grubb Knight Frank:

“I don’t think the housing market is overheated based on demand and supply fundamentals.”

Mark Dotzour, Chief Economist, Real Estate Center, Texas A&M University:

“We are not in a housing bubble. We are in a situation where demand for houses is much higher than supply.”

Calvin Schnure, SVP of Research & Economic Analysis, NAREIT:

“Given all the demand and little supply the residential market is FAR from overheated.”

Bottom Line

Currently, there is an imbalance between supply and demand for housing. This has created a natural increase in values not a bubble in prices. Don’t let the imbalance bubble to get you, CALL us today 786.554.8063 or email us at George@GeorgeAssal.com, you know you can count on our help every step of the way while reaching your goal faster, easier and with a smile on your face.