http://realty.wistia.com/medias/ar313gm83w?embedType=async&videoWidth=800

dade

Sales Dropped last month …

On December 22nd 2015, the National Association of Realtors (NAR) released their latest Existing Home Sales Report which covered sales in November. The report revealed that sales:

“…fell 10.5 percent to a seasonally adjusted annual rate of 4.76 million in November (lowest since April 2014 at 4.75 million)…”

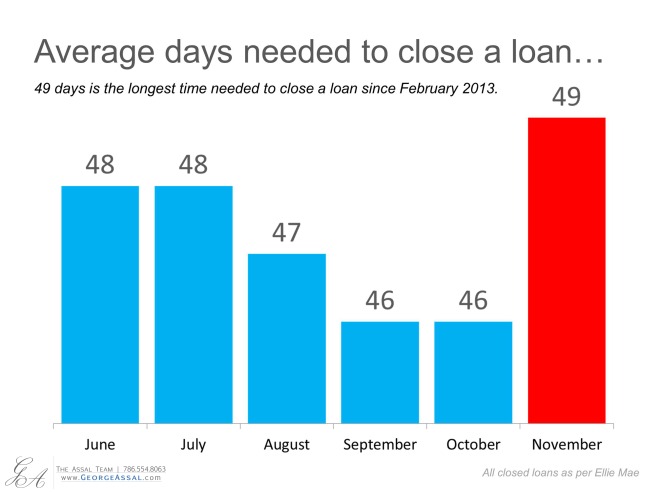

That revelation gave birth to a series of industry articles, some of which quoted pundits questioning whether the housing market was slowing. In actuality, there is one rather simple explanation to much of the falloff in sales last month. It is likely the implementation of the “Know Before You Owe” mortgage rule, commonly known as the TILA-RESPA Integrated Disclosure (TRID) rule, which went into effect on October 3. These regulations caused house closings to be delayed by an extra three days in November as shown in the graph below.

Three days might sound like a minimal difference. However, since there are only approximately 20 days in a month that a closing would normally take place (Mondays through Fridays), losing three days constitutes well over 10% of all closings. These sales are not lost. They are just moved into the next month’s numbers. In a DS News article on the subject also posted on December 22nd, Auction.com EVP Rick Sharga explained:

“The most likely cause for the weak sales numbers is a delay in processing loans due to the new TRID mortgage requirements imposed by the CFPB. This is the biggest change in mortgage document processing in many years, and there have been numerous reports within the industry of problems implementing the process and the new documentation that comes with it.”

So how is the housing market actually doing?

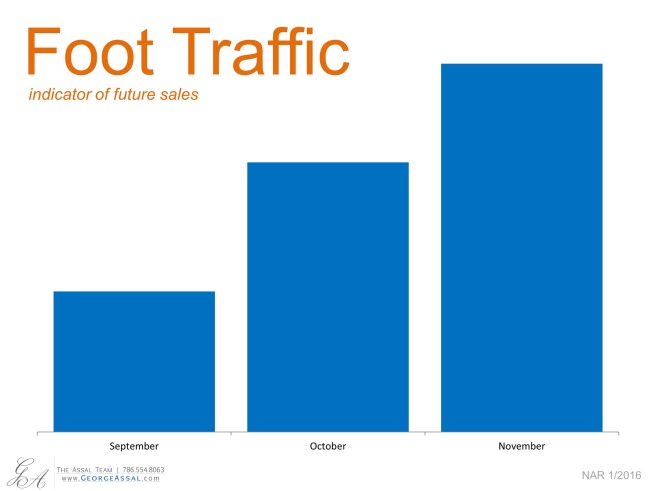

A better way to look at how well the housing market is doing is to look at the Foot Traffic Report from NAR which quantifies the number of prospective buyers that are actively looking for a home at the current time:

We can see immediately that demand to buy single family homes is increasing over the last few months – not decreasing.

Bottom Line

No matter what last month’s sales numbers show, the housing market is still doing well as demand remains strong.

Call 786.554.8063 or email us George@GeorgeAssal.com, WE are here to facilitate and help you during the process of buying, selling, or renting any real estate needs, which will result in reaching your financial goals quickly and with ease, visit our page www.GeorgeAssal.com .

Single Family Home Sales – Monthly Market Summary: March 2013

Single Family Home Sales – Monthly Market Summary: March 2013

I am a Miami-Dade real estate specialist. If you would like to schedule a buyer or seller meeting with me, please feel free to call me directly at 786.554.8063 or via email George@GeorgeAssal.com

If you are still thinking whether is a good time to buy or not, here is an article posted by National Association of Realtors

April Existing-Home Sales Up, Prices Rise Again

WASHINGTON (May 22, 2012) – Existing-home sales rose in April and remain above a year ago, while home prices continued to rise, according to the National Association of Realtors®. The improvements in sales and prices were broad based across all regions.

Total existing-home sales1, which are completed transactions that include single-family homes, townhomes, condominiums and co-ops, increased 3.4 percent to a seasonally adjusted annual rate of 4.62 million in April from a downwardly revised 4.47 million in March, and are 10.0 percent higher than the 4.20 million-unit level in April 2011.

Lawrence Yun, NAR chief economist, said the housing recovery is underway. “It is no longer just the investors who are taking advantage of high affordability conditions. A return of normal home buying for occupancy is helping home sales across all price points, and now the recovery appears to be extending to home prices,” he said. “The general downtrend in both listed and shadow inventory has shifted from a buyers’ market to one that is much more balanced, but in some areas it has become a seller’s market.”

Total housing inventory at the end of April rose 9.5 percent to 2.54 million existing homes available for sale, a seasonal increase which represents a 6.6-month supply2 at the current sales pace, up from a 6.2-month supply in March. Listed inventory is 20.6 percent below a year ago when there was a 9.1-month supply; the record for unsold inventory was 4.04 million in July 2007.

“A diminishing share of foreclosed property sales is helping home values. Moreover, an acute shortage of inventory in certain markets is leading to multiple biddings and escalating price conditions,” Yun said. He notes some areas with tight supply include the Washington, D.C., area; Miami; Naples, Fla.; North Dakota; Phoenix; Orange County, Calif.; and Seattle. “We expect stronger price increases in most of these areas.”

The national median existing-home price3 for all housing types jumped 10.1 percent to $177,400 in April from a year ago; the March price showed an upwardly revised 3.1 percent annual improvement. “This is the first time we’ve had back-to-back price increases from a year earlier since June and July of 2010 when the gains were less than one percent,” Yun said. “For the year we’re looking for a modest overall price gain of 1.0 to 2.0 percent, with stronger improvement in 2013.”

Distressed homes4 – foreclosures and short sales sold at deep discounts – accounted for 28 percent of April sales (17 percent were foreclosures and 11 percent were short sales), down from 29 percent in March and 37 percent in April 2011. Foreclosures sold for an average discount of 21 percent below market value in April, while short sales were discounted 14 percent.

NAR President Moe Veissi, broker-owner of Veissi & Associates Inc., in Miami, said home buyers should look into financing in the early stages of their search process. “With the tight lending environment it’s a good idea to consult with a Realtor® about mortgages and program options in your area, and tips for boosting your credit score well in advance of making an offer on a home,” he said. “It helps to go into the process knowing what it takes to succeed.”

According to Freddie Mac, the national average commitment rate for a 30-year, conventional, fixed-rate mortgage declined to 3.91 percent in April from 3.95 percent in March; the rate was 4.84 percent in April 2011. Last week the 30-year fixed rate dropped to a record weekly low of 3.79 percent; recordkeeping began in 1971.

First-time buyers rose to 35 percent of purchasers in April from 33 percent in March; they were 36 percent in April 2011.

All-cash sales fell to 29 percent of transactions in April from 32 percent in March; they were 31 percent in April 2011. Investors, who account for the bulk of cash sales, purchased 20 percent of homes in April, compared with 21 percent in March and 20 percent in April 2011.

Single-family home sales rose 3.0 percent to a seasonally adjusted annual rate of 4.09 million in April from 3.97 million in March, and are 9.9 percent higher than the 3.72 million-unit pace a year ago. The median existing single-family home price was $178,000 in April, up 10.4 percent from April 2011.

Existing condominium and co-op sales increased 6.0 percent to a seasonally adjusted annual rate of 530,000 in April from 500,000 in March, and are 10.4 percent above the 480,000-unit level in April 2011. The median existing condo price was $172,900 in April, which is 8.1 percent above a year ago.

Regionally, existing-home sales in the Northeast rose 5.1 percent to an annual level of 620,000 in April and are 19.2 percent higher than a year ago. The median price in the Northeast was $256,600, up 8.8 percent from April 2011.

Existing-home sales in the Midwest increased 1.0 percent in April to a pace of 1.03 million and are 14.4 percent above April 2011. The median price in the Midwest was $141,400, up 7.4 percent from a year ago.

In the South, existing-home sales rose 3.5 percent to an annual level of 1.79 million in April and are 6.5 percent higher than a year ago. The median price in the South was $153,400, up 8.0 percent from April 2011.

Existing-home sales in the West increased 4.4 percent to an annual pace of 1.18 million in April and are 7.3 percent above April 2011. The median price in the West was $221,700, a surge of 15.9 percent from a year ago.

The National Association of Realtors®, “The Voice for Real Estate,” is America’s largest trade association, representing 1 million members involved in all aspects of the residential and commercial real estate industries.

If you are considering listing your Brickell, Coconut Grove, Coral Gables, Pinecrest, Palmetto Bay, Doral, Miami Shores, Miami-Dade property for sale or rent please don’t hesitate to contact me. The market is changing and I would be happy to discuss the current value of your home with you. I can be reached on my cell at 786.554.8063

Shopping for a Real Estate Agent? Thinking of Selling/Buying?

Contact me

George R. Assal| Realtor–Associate® | BBF Member | Property Manager |

REO & Short Sale Specialist

English- Español EWM Realtors® | A Home Services of America Company |

An Affiliate of Berkshire Hathaway

C: 786.554.8063|O: 305.329.7635|F: 888.240.5507| george@georgeassal.com |www.georgeassal.com