Can Creditors Collect Information Beyond The 6 Required Pieces? In addition to the required pieces – Name Income Social Security Number Property Address Estimated Property Value and Mortgage Amount sought – a creditor may collect whatever additional information they deem necessary. However, as soon as you have provided the 6 required pieces, the creditor has 3 business days to provide a Loan Estimate for approved loans.

What 6 Pieces of Information Make A TRID Loan Application? Submitting these 6 pieces of information – Name Income Social Security Number Property Address Estimated Value of Property and Mortgage Loan Amount sought – constitutes a valid loan application under the TRID rule. You may apply and submit these in writing OR in oral form; a live conversation, or a phone call, backed by a written record of the conversation is a legitimate application. Once these 6 pieces of information are submitted a creditor MUST supply a Loan Estimate for approved loans within 3 business days.

Like the guy in the video says, the two do not really compare at all. The one advantage of renting is being generally free of most maintenance responsibilities. But by renting, you lose the chance to build equity take advantage of tax benefits and protect yourself against rent increases.Also, you may be at the mercy of the landlord for housing. Owning a home has many benefits. When you make a mortgage payment, you are building equity increasing YOUR net worth. Owning a home also qualifies you for tax breaks that assist you in dealing with your new financial responsibilities like insurance, real estate taxes, and upkeep which can be substantial. But given the freedom, stability, and security of owning your own home they are worth it.

On December 22nd 2015, the National Association of Realtors (NAR) released their latest Existing Home Sales Report which covered sales in November. The report revealed that sales:

“…fell 10.5 percent to a seasonally adjusted annual rate of 4.76 million in November (lowest since April 2014 at 4.75 million)…”

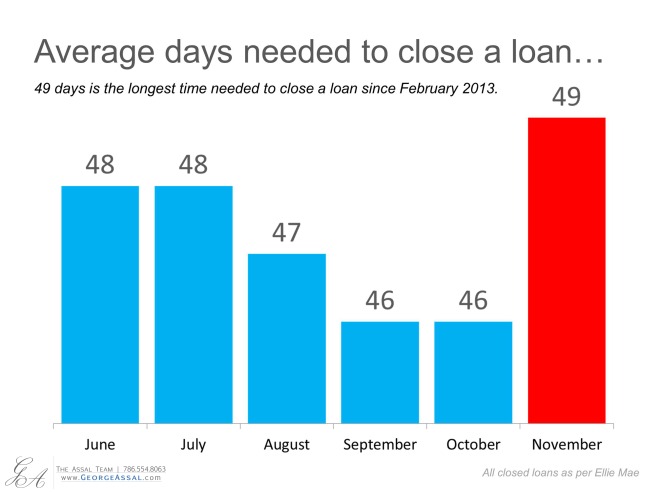

That revelation gave birth to a series of industry articles, some of which quoted pundits questioning whether the housing market was slowing. In actuality, there is one rather simple explanation to much of the falloff in sales last month. It is likely the implementation of the “Know Before You Owe” mortgage rule, commonly known as the TILA-RESPA Integrated Disclosure (TRID) rule, which went into effect on October 3. These regulations caused house closings to be delayed by an extra three days in November as shown in the graph below.

Three days might sound like a minimal difference. However, since there are only approximately 20 days in a month that a closing would normally take place (Mondays through Fridays), losing three days constitutes well over 10% of all closings. These sales are not lost. They are just moved into the next month’s numbers. In aDS News article on the subject also posted on December 22nd, Auction.com EVP Rick Sharga explained:

“The most likely cause for the weak sales numbers is a delay in processing loans due to the new TRID mortgage requirements imposed by the CFPB. This is the biggest change in mortgage document processing in many years, and there have been numerous reports within the industry of problems implementing the process and the new documentation that comes with it.”

So how is the housing market actually doing?

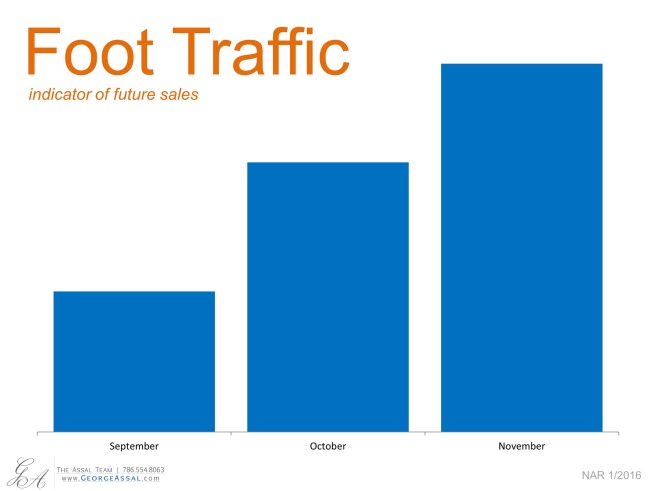

A better way to look at how well the housing market is doing is to look at the Foot Traffic Report from NAR which quantifies the number of prospective buyers that are actively looking for a home at the current time:

We can see immediately that demand to buy single family homes is increasing over the last few months – not decreasing.

Bottom Line

No matter what last month’s sales numbers show, the housing market is still doing well as demand remains strong.

Call 786.554.8063 or email us George@GeorgeAssal.com, WE are here to facilitate and help you during the process of buying, selling, or renting any real estate needs, which will result in reaching your financial goals quickly and with ease, visit our page www.GeorgeAssal.com .

Last week, an article in the Washington Post discussed a new ‘threat’ homebuyers will soon be facing: higher mortgage rates. The article revealed:

“The Mortgage Bankers Association expects that rates on 30-year loans could reach 4.8 percent by the end of next year, topping 5 percent in 2017. Rates haven’t been that high since the recession.”

How can this impact the housing market?

The article reported that recent analysis from Realtor.com found that –

“…as many as 7% of people who applied for a mortgage during the first half of the year would have had trouble qualifying if rates rose by half a percentage point.”

This doesn’t necessarily mean that those buyers negatively impacted by a rate increase would not purchase a home. However, it would mean that they would either need to come up with substantially more cash for a down payment or settle for a lesser priced home.

Below is a table showing how a jump in mortgage interest rates would impact the purchasing power of a prospective buyer on a $300,000 home.

In Conclusion

If you are considering a home purchase (either as a first time buyer or move-up buyer), purchasing sooner rather than later may make more sense from a pure financial outlook.

Tired of being a tenant? thinking of selling your home?, looking to upgrade? 1st time buyer(s)? buying your dream home? Call us 786.554.8063 or email us George@GeorgeAssal.com, WE are here to facilitate and help you during the process of buying, selling, or renting any real estate needs, which will result in reaching your financial goals quickly and with ease, visit our page www.GeorgeAssal.com

I am a Miami-Dade real estate specialist. If you would like to schedule a buyer or seller meeting with me, please feel free to call me directly at 786.554.8063 or via email George@GeorgeAssal.com