http://realty.wistia.com/medias/ar313gm83w?embedType=async&videoWidth=800

SouthFlorida

Sales Dropped last month …

On December 22nd 2015, the National Association of Realtors (NAR) released their latest Existing Home Sales Report which covered sales in November. The report revealed that sales:

“…fell 10.5 percent to a seasonally adjusted annual rate of 4.76 million in November (lowest since April 2014 at 4.75 million)…”

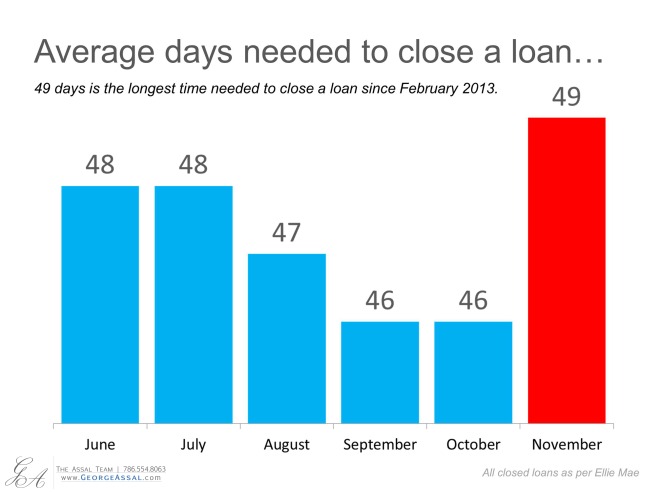

That revelation gave birth to a series of industry articles, some of which quoted pundits questioning whether the housing market was slowing. In actuality, there is one rather simple explanation to much of the falloff in sales last month. It is likely the implementation of the “Know Before You Owe” mortgage rule, commonly known as the TILA-RESPA Integrated Disclosure (TRID) rule, which went into effect on October 3. These regulations caused house closings to be delayed by an extra three days in November as shown in the graph below.

Three days might sound like a minimal difference. However, since there are only approximately 20 days in a month that a closing would normally take place (Mondays through Fridays), losing three days constitutes well over 10% of all closings. These sales are not lost. They are just moved into the next month’s numbers. In a DS News article on the subject also posted on December 22nd, Auction.com EVP Rick Sharga explained:

“The most likely cause for the weak sales numbers is a delay in processing loans due to the new TRID mortgage requirements imposed by the CFPB. This is the biggest change in mortgage document processing in many years, and there have been numerous reports within the industry of problems implementing the process and the new documentation that comes with it.”

So how is the housing market actually doing?

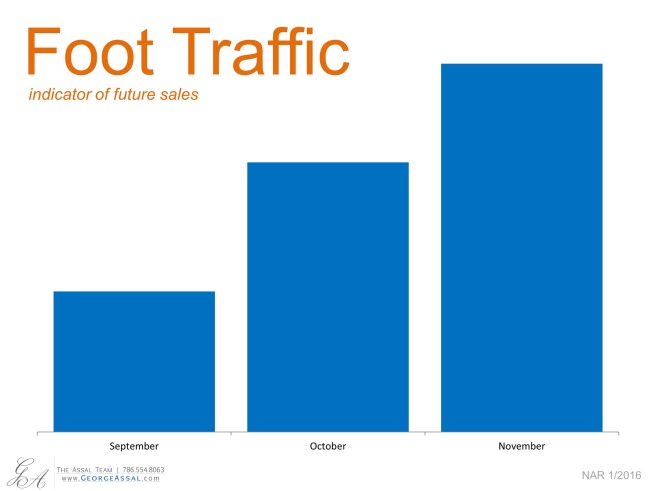

A better way to look at how well the housing market is doing is to look at the Foot Traffic Report from NAR which quantifies the number of prospective buyers that are actively looking for a home at the current time:

We can see immediately that demand to buy single family homes is increasing over the last few months – not decreasing.

Bottom Line

No matter what last month’s sales numbers show, the housing market is still doing well as demand remains strong.

Call 786.554.8063 or email us George@GeorgeAssal.com, WE are here to facilitate and help you during the process of buying, selling, or renting any real estate needs, which will result in reaching your financial goals quickly and with ease, visit our page www.GeorgeAssal.com .

Homeownership is the Key to Well-Being in Retirement

There has been much talk about homeownership and whether it is a true vehicle for building wealth. A new report looks at the impact owning a home has on the financial wellbeing of people closing in on their retirement years (ages 55-64).

In recently study by the Hamilton Project, Ten Economic Facts about Financial Well-Being in Retirement, it was revealed that:

1. Middle-class households near retirement age have about as much wealth in their homes as they do in their retirement accounts.

“Over the past quarter century the largest single source of wealth for all but the richest households nearing retirement age has been their homes, which accounted for about two-fifths of net worth in the early 1990s and accounts for about one-third today.”

2. Home equity is a very important source of net worth to all but the wealthiest households near retirement age.

“Home equity is an important source of wealth for middle income households, accounting for more than one-third of total net worth for the second, third, and fourth quintiles of the net worth distribution… The fifth quintile has a much larger share in business equity—almost a quarter—than any other quintile. (The figure leaves out the bottom quintile of households because they have negative net worth. It is likely that these households will rely almost exclusively on Social Security in retirement.)”

Here is an asset breakdown for the middle 20% of Americans determined by median net worth ($165, 720):

Obviously, the data again proves that homeownership has a big role in building wealth for American families

Are you prepared to retire and ready to start a new life? YES?, We the ASSAL team are here to help you reach your goal faster, easier and with a smile on your face while planning your future. Call us today at 786.554.8063 or send us an email at george@georgeassal.com– you can count on our help every step.

Is now a good time to Rent? Definitely NOT!

People often ask us whether or not now is a good time to buy a home. No one ever asks when a good time to rent is. However, we want to make certain that everyone understands that today is NOT a good time to rent.

The Census Bureau just released their second quarter median rent numbers.

Here is a graph showing rent increases from 1988 until today:

At the same time, a report by Axiometrics revealed:

“The national apartment market’s annual effective rent growth rate of 5.1% in June 2015 represented a 47-month high, and continued a streak of 5.0%-plus rent growth that is now the longest in at least six years, according to apartment market research. The effective rent growth in June 2014 was 3.7%, putting June 2015’s exceptional performance into perspective.

This is the highest rate since the 5.3% of July 2011. The metric has reached at least 5.0% for five straight months, the longest such streak since Axiometrics started monthly reporting of annual apartment data in April 2009.”

Where will rents be headed in the future?

Stephanie McCleskey, Axiometrics vice president of research, commented on the above report in an article by Real Estate Economy Watch:

“Rent growth is just shy of the post-recession peak, and the June metrics reflect the continued strength of the apartment market. The demand for apartments is still strong, despite the record number of new units being delivered this year. Tight occupancy is why landlords can push rents higher.”

Bottom Line

Tired of paying rent? Are you ready, willing and able to start a new life? if you answered YES, now may make sense, it might not be a good time to rent however is a good time to buy, We (the ASSAL team) are not for rent nor for sale but YES to help you reach your goal faster, easier and with a smile on your face! Call us today at 786.554.8063 or send us an email at george@georgeassal.com– you can count on our help every step of the way.

What is a Housing Bubble? Is One Forming?

The recent talk of Greece and its financial challenges has some questioning whether the U.S. could also return to the crisis we experienced in 2008. Some are looking at the rise in real estate values and wondering whether we are in the middle of another housing price bubble.

What actually is a price bubble?

Here is the definition according to Jack M. Guttentag, Professor of Finance Emeritus at the Wharton School of the University of Pennsylvania:

“A price bubble is a rise in price based on the expectation that the price will rise. Sooner or later something happens to erode confidence in continued price increases, at which point the bubble bursts and prices drop. What makes it a price bubble is that the cause of the price increase is an expectation that the price will increase, which sooner or later must reverse itself.”

Does Professor Guttentag believe we are in another housing bubble?

In a recent article, he explained:

“My view is that we are a long way from another house price bubble. Home buyers, lenders, investors and regulators now understand that a nationwide decline in house prices is possible — because we recently lived through one.”

What are home prices doing?

Though home values are continuing to appreciate, the acceleration of the increases has slowed to year-over-year numbers which reflect a healthy housing market. Here is a chart showing year-over-year appreciation since January of last year:

We can see that appreciation rates have dropped from double digit numbers to more normal rates of 5% or lower.

Bottom Line

We think Nick Timiraos of the Wall Street Journal put it best in a recent tweet:

“Predictions of a new national home price bubble look unfounded for now, according to data.”

Interested in selling your home or looking to buy one, give us a call today at 786.554.8063 or send us an email at george@georgeassal.com. We will look forward to hearing from you!