http://realty.wistia.com/medias/ar313gm83w?embedType=async&videoWidth=800

The Roads Real Estate

The Impact of Higher Interest Rates

Last week, an article in the Washington Post discussed a new ‘threat’ homebuyers will soon be facing: higher mortgage rates. The article revealed:

“The Mortgage Bankers Association expects that rates on 30-year loans could reach 4.8 percent by the end of next year, topping 5 percent in 2017. Rates haven’t been that high since the recession.”

How can this impact the housing market?

The article reported that recent analysis from Realtor.com found that –

“…as many as 7% of people who applied for a mortgage during the first half of the year would have had trouble qualifying if rates rose by half a percentage point.”

This doesn’t necessarily mean that those buyers negatively impacted by a rate increase would not purchase a home. However, it would mean that they would either need to come up with substantially more cash for a down payment or settle for a lesser priced home.

Below is a table showing how a jump in mortgage interest rates would impact the purchasing power of a prospective buyer on a $300,000 home.

In Conclusion

If you are considering a home purchase (either as a first time buyer or move-up buyer), purchasing sooner rather than later may make more sense from a pure financial outlook.

Tired of being a tenant? thinking of selling your home?, looking to upgrade? 1st time buyer(s)? buying your dream home? Call us 786.554.8063 or email us George@GeorgeAssal.com, WE are here to facilitate and help you during the process of buying, selling, or renting any real estate needs, which will result in reaching your financial goals quickly and with ease, visit our page www.GeorgeAssal.com

Rent vs. Buy: Either Way You’re Paying A Mortgage

There are some people that have not purchased a home because they are uncomfortable taking on the obligation of a mortgage. Everyone should realize that, unless you are living with your parents rent free, you are paying a mortgage – either your mortgage or your landlord’s.

As The Joint Center for Housing Studies at Harvard University explains:

“Households must consume housing whether they own or rent. Not even accounting for more favorable tax treatment of owning, homeowners pay debt service to pay down their own principal while households that rent pay down the principal of a landlord plus a rate of return.

That’s yet another reason owning often does—as Americans intuit—end up making more financial sense than renting.”

Christina Boyle, a Senior Vice President, Head of Single-Family Sales & Relationship Management at Freddie Mac, explains another benefit of securing a mortgage vs. paying rent:

“With a 30-year fixed rate mortgage, you’ll have the certainty & stability of knowing what your mortgage payment will be for the next 30 years – unlike rents which will continue to rise over the next three decades.”

As an owner, your mortgage payment is a form of ‘forced savings’ that allows you to have equity in your home that you can tap into later in life. As a renter, you guarantee your landlord is the person with that equity.

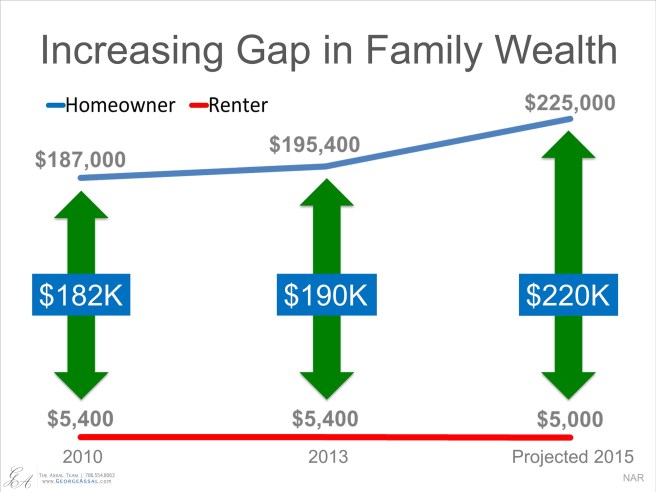

The graph below shows the widening gap in net worth between a homeowner and a renter:

In Conclusion

Whether you are looking for a primary residence for the first time or are considering a vacation home on the shore, owning might make more sense than renting with home values and interest rates projected to climb.

Tired of renting and/or being a Tenant(s)? Thinking of selling your home?, looking to upgrade?, First Time buyer(s)? Buying your dream home this year? Call us 📞786.554.8063 or 📧George@GeorgeAssal.com, WE are here to facilitate and help you during the process of buying, selling or renting any real estate needs, which will result in reaching your financial goals quickly and with ease. 💻 http://www.GeorgeAssal.com

BRICKELL ROADS TOWNHOUSE – FOR SALE

*** LOCATION – LOCATION – LOCATION ***

240 SW 15th RD #105 Miami FL 33133

Rare opportunity to own this unique 3 story corner unit with laminated wood floors, open kitchen, 2 assigned parking spaces, full bedroom at the entry level, walk-in closets, high ceilings with interesting angled walls, (not your typical boring rectangular room), this unit has the largest backyard, centrally located, pet friendly and gated community, most important… seller motivated. Asking $350,000.00

Interested in Selling, Buying, Renting in Brickell, Downtown, Coconut Grove, Coral Gables and surrounding areas? Call me 786.554.8063 or email me George@GeorgeAssal.com, I can help, because working with someone who knows the numbers and area is crucial.